Let E1, E2,

…, Ej(j =

0, 1, 2, …) represent the exhaustive and mutually exclusive outcomes

(states) of a system at any time. Initially, at time t0,

the system may be in any of these states. Let

aj(0)(j

= 1, 2, …) be the absolute probability that the system is in state

Ej at t0.

Assume further that the system is Markovian.

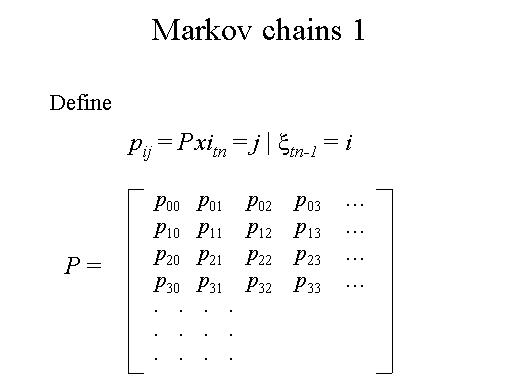

Define the following as the one-step transition probability of going from

state i at tn-1 to state

j and tn and assume that

these probabilities are stationary over time. The transition probabilities

from state E1 to state Ej

can be more conveniently arranged in a matrix form as follows.